Date: January 29, 2024

Category: Newsletter

Happy New Year 🎉 – ok, that’s the last time you will hear it from me this year 😉

2024 is very much underway, and is it just me, but it’s been a busy month!

This month, we have seen inflation numbers increase, the Bank of Canada hold prime (as expected), and we are finally seeing the 5-year fixed rate come down.

Dare I mention that last week, we saw a 5-year fixed rate in the 4% range! Hang onto your hats; it will be a fun ride this year.

Here is a quick recap of where things are and some items for perspective.

- As of this month, experts believe the Bank of Canada’s📉 first rate cut can arrive as early as March 🍀, with an additional four .25% cut before the end of the year. Given that we still have seven more rate announcements this year, at this point, it’s anyone’s guess, and things can also change quickly. The reality is the rates will have to come down, or we will go into recession, but it will take time; this will be the epitome of slow and steady🐌.

- Single-family housing🏡 has become a rare commodity. The number of permits issued for single-family homes in Canada has fallen to levels last seen in early 1980. This leads us to believe that single-family homes will soon become unattainable to future generations

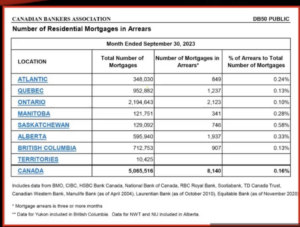

There’s no argument; we are feeling the pinch. When we are in a higher-rate market, there is always much talk about mortgage delinquencies, so let’s set the record straight and give you some perspective. Ontario holds the most mortgages in Canada, with 2,194,643 mortgages, of which only 2,123 or .10% are currently in arrears. For perspective, Canada has 5,065,516 mortgages and 8,140 mortgages in arrears, with only a .16% total nationally. (this is based on information provided by the Canadian Bankers Association). It’s interesting to note that the deficiencies are lower in Ontario and BC, where home prices are higher, and delinquencies are higher in provinces where the home prices are lower. What does that mean?

There’s no argument; we are feeling the pinch. When we are in a higher-rate market, there is always much talk about mortgage delinquencies, so let’s set the record straight and give you some perspective. Ontario holds the most mortgages in Canada, with 2,194,643 mortgages, of which only 2,123 or .10% are currently in arrears. For perspective, Canada has 5,065,516 mortgages and 8,140 mortgages in arrears, with only a .16% total nationally. (this is based on information provided by the Canadian Bankers Association). It’s interesting to note that the deficiencies are lower in Ontario and BC, where home prices are higher, and delinquencies are higher in provinces where the home prices are lower. What does that mean? - It has been reported that insolvencies are on the rise. This means personal bankruptcies and consumer proposals. What’s important about this stat is many don’t know if you currently own a home; you can go through insolvency and still keep your home. Insolvency does not equal homelessness or mortgage arrears. If you find yourself at this crossroads, please talk to us. No judgement, just help.

- Over half of Canadian businesses expect inflation to average over 3% for the next two years. This will directly have an impact on the prime rate and the Bank of Canada’s decision to lower the prime slowly.

- Payment shock is of concern to most lenders. This is when your current mortgage term ends, and you take on a new mortgage with a higher rate, thus giving you a payment shock. We can avoid this…if you’ve been reading my updates, I’ve been preaching this for years, and most often in the last few updates. Let’s connect to review. If your rate increases by double, this does NOT mean your payment will double.

January’s 🎯 Action Items

This will be a pivotal year for many of us, with 35% of all mortgages coming due in 2024, and so each month, I will leave you with one ACTION ITEM in hopes that this will help you manage 2024 a little easier.

If you are purchasing a new home this year and are a FIRST-TIME HOME BUYER.

- If your down payment is sitting in a savings account and you are still looking for a home. Consider moving those funds to an RRSP and utilizing the First Time Buyer Plan, which allows you to borrow that same money back from yourself (up to $35,000) with no penalty. Doing this means you must pay that $35,000 back to yourself over the next 15 years or add that income to your yearly taxes. It also means that you will likely receive a tax rebate that you can use to help offset the costs of moving, purchasing furniture, etc. Remember, the funds must be in your RRSP for 90 days before you can remove them to purchase your new home.

If you were a first-time home buyer in 2023

- don’t forget to let your accountant know you purchased a new home in 2023 and apply for the First Time Buyer Tax credit of up to $1,500 per first-time home buyer.

If your mortgage is up for renewal between now and June 2024.

- I know you are tired of hearing me say this, but please connect with me so we can review your options. This is not a sales pitch but an opportunity to save money. For example, I’m speaking with clients being offered rates over 6% when we can get them into rates in the low 5% range. It doesn’t cost you to review your options.

Let’s Celebrate!

We know it’s very early, but we are planning our 2024 Client and Partner Appreciation Event, and so each month, we will give you a little more information about our plans for this year.

Hint- there will be food 🍲🍕🍰, drinks 🍹, music 🎶, and photos 📸 😉 🎉

Mortgages can be complicated; we are here to help you make “cents” of it.

We focus on Mortgage Solutions, Period!

To learn more connect with Ana Cruz 905.870.0513 or email at ana@askanacruz.ca