Date: February 27, 2023

Category: Newsletter

Has this been the quickest two months, or is it just me?

So far, in 2023, we’ve seen the following; our first Bank of Canada (BOC) increase, the five-year fixed rates roller coaster, inflation numbers have dropped, and qualifying for a mortgage has become even harder so let’s unpack all that and talk about where we are heading.

We had our first Bank of Canada (BOC) increase in January. The next increase is scheduled for March 8th, and there are mixed reviews on what the BOC will do. Let’s consider this information and try to understand what will happen in March.

In January, the US inflation rates climbed by .50%. We expected to see about 15,000 new jobs added to the Canadian economy; however, we saw about ten times that at 150,000 new jobs – most full-time. These two things alone may result in the BOC pause being short-lived.

Over the last two weeks, bond yields have increased by over .50%. This is important as the bond market indicates what will happen to fixed rates. Typically there is about a 1.20%-1.50% spread between the 5-year bond rate and the 5-year fixed mortgages with typically a 2-3 day lead time to see the changes in the 5-year fixed rate.

Quick insert – you’ve heard me say it’s not all about the rate and that’s still true; let me explain. If you have two lenders where one is a bank and the other is a non-bank, and the rate is .05% higher with the non-bank, many people will default to going with the bank; however, the difference in the .05% is sometimes less than a cup of a coffee a month over the term. What is often missed here is if rates go down and you need to break that 5-year fixed bank mortgage, you are likely paying a three to five times higher penalty to break the same mortgage.

We are seeing the five-year rates increase, so I urge you to connect with us if you are up for renewal in the next year so we can discuss your options and lock in a rate.

There are mixed reviews on what the BOC will do in March; however, if you listen to what Tiff Macklhem recently said, he’s prepared to raise rates further if necessary, and there are no plans to lower rates just yet. The pause we’ve all heard about is an opportunity to give time to time and collect data.

Here’s Tiff’s most recent statement, “I want to be very clear; we are pausing interest rate hikes to assess whether we raised interest rates enough to get inflation all the way back to target. Monetary Policy works with the lag. We’ve raised rates rapidly. We’re seeing the effects. We know there’s more to come. It makes sense to pause and assess whether we’ve done enough.”

My thoughts on BOC increases and predictions (I hate predicting) are that we will pause slightly (possibly no increase in March) while waiting for the data to catch up. We will still see another rate increase or two before the end of the year, then a possible levelling off, but it won’t be until 2024 that we see any drop in the overnight rate. We’ve all heard Tiff’s statement from 2020 when he said rates would stay low for an extended period – fast forward to 2021 🤷🏼♀️. My opinion is that this is his attempt at transparency.

Again, I’m not too fond of predictions, and I make this statement based on the information available today…so let’s talk next month.

I’ve addressed the five-year fixed rates, and there’s little to discuss when dealing with the current variable rates, as not much has changed.

However, let’s talk about qualifying for a mortgage currently. Regardless if you are purchasing a home, renewing or refinancing your current mortgage, everyone needs to qualify using the stress test. Ah, the much-hated stress test that has saved so many people over the last few months. I’m not a fan of the stress test for the most part as I think it’s too high; however, I fully support the idea of a stress test. For those upset about having to qualify at 2% higher than the rate they took, now you are likely thanking the stress test too.

Fast forward to today and the current stress test effects. Many clients with good income and credit struggle to qualify for a mortgage with the current stress test in place – why do I mention this?

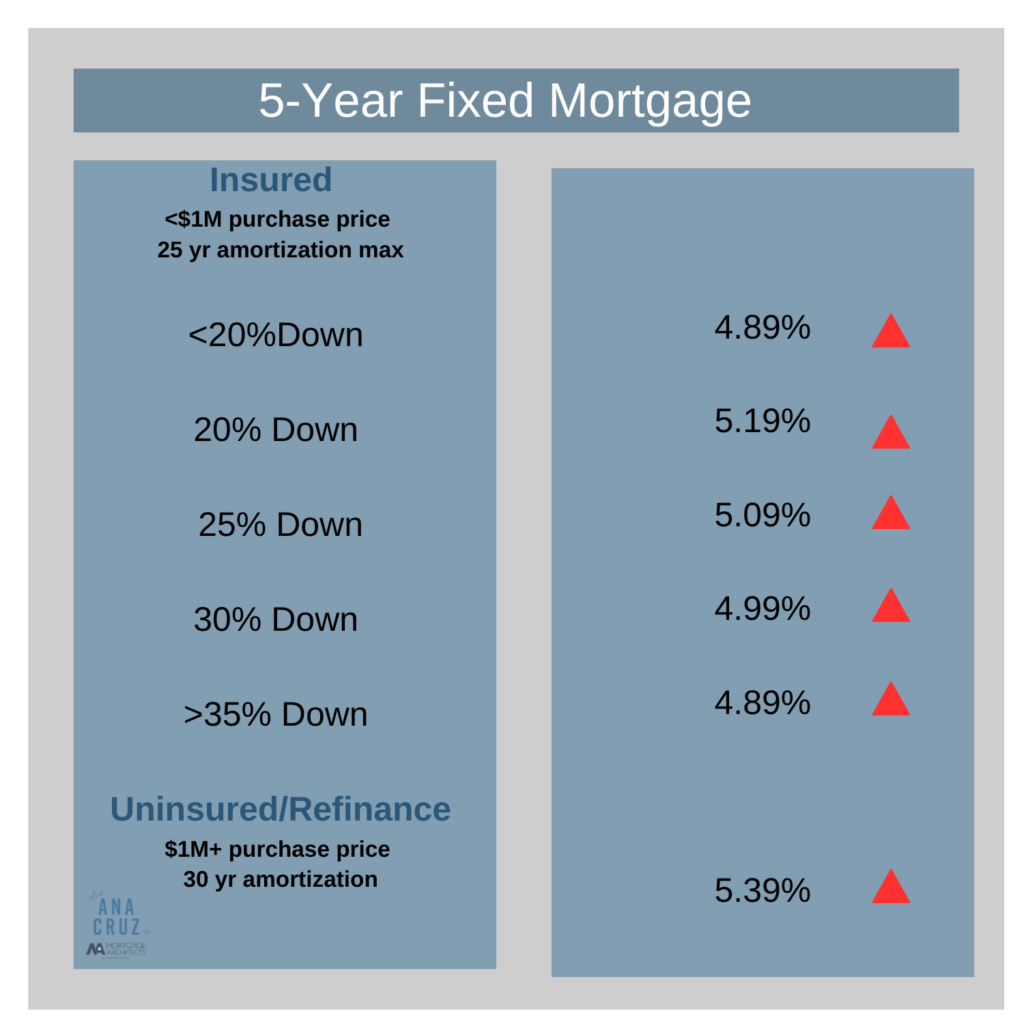

As you can see from the graph below, the five-year fixed rates are on the rise, and yet, they are lower than the five-year variable rates. If you are planning on making any changes to your current mortgage (renewal/refinance) or looking to purchase a new home, connect with us ASAP so we can lock in your rate and your qualifying rate. If rates go down – you are in a better position, and we will get you the lower rate, but if rates go up and you were already tight in qualifying, now we have you locked in for 120 days.

Amid all the talk about higher rates and payments, it’s important to note that mortgage delinquencies are not necessarily up or expected to rise. Of course, like everything in this newsletter – this is based on the information we have available today.

If you made it this far, I would also like to send you a HUGE virtual hug and THANK YOU for your continued trust and loyalty. This has allowed us to once again receive the Mortgage Architect’s Gold Presidents Club Award, which is only accepted by the top 7% of our company. THANK YOU; your trust humbles me.

Thank you to all that connect with me regularly and give me feedback on these newsletters. A lot of work goes into them and I’m thrilled to hear that you take the time to read them. Remember caring is sharing – send this to a friend

Ask Ana Cruz:

Q- If my mortgage is up for renewal later this year, when do I need to connect with you?

A- It’s never to early to have a conversation.

We may not do anything until we are about 4.5 months to your renewal date, but it’s the right time to start planning now.

Mortgages can be complicated; we are here to help you make “cents” of it.

We focus on Mortgage Solutions, Period!

To learn more connect with Ana Cruz 905.870.0513 or email at ana@askanacruz.ca